1. There are many laser application scenarios and the downstream industry chain is huge

Laser (Laser, Light Amplification by Stimulated Emission of Radiation) refers to the light generated by the stimulated radiation of atoms. It is a kind of coherent light radiation with high energy density, good directivity and monochromaticity. The principle of laser generation is that when the electrons in the atom absorb energy and then transition from a low energy level to a high energy level, and then fall from a high energy level to a low energy level, the released energy is released in the form of photons.

The downstream market of laser equipment is large and complex, forming a complete industrial chain. At present, laser-related products and services have spread all over the world, forming a rich and huge laser industry. The application fields of laser include material processing, information communication, data storage, medical beauty, scientific research and military, instrument sensing, display, additive manufacturing and other subdivision fields, forming a rich and huge industry and a complete industrial chain. The upstream of the industrial chain mainly includes optical materials and optical components, the middle reaches of various lasers and supporting equipment, the downstream is mainly laser application products, and the downstream applications penetrate into consumer electronics, high-end materials, semiconductor processing, automobiles, ships, communications, and medical care. Beauty, military and many other fields.

Due to the complex downstream industries involved, international leaders focus on expanding their business territory through mergers and acquisitions. In 2018, the operating income of leading international laser companies, such as TRUMPF, the United States, IPG, and II, achieved rapid growth. Because the downstream laser equipment is more complicated, in order to expand the business blueprint, leading foreign companies have adopted mergers and acquisitions to expand-TRUMPF acquired Amphos to strengthen its layout in the field of ultrafast lasers; Coherent acquired Ondax , To expand the product portfolio of components, lasers and laser systems; IPG acquired Genesis and entered the field of robotics (10.840, -0.27, -2.43%) automation.

2. Laser is the core component of laser equipment, fiber laser has obvious advantages

(1) The laser is composed of three parts: pump source, gain medium, and resonant cavity

Laser is the core component of laser equipment. Laser is the light-emitting device of laser equipment. As the most critical component of laser equipment, the technical barriers in this link are relatively high. The laser is mainly composed of three parts: pump source, gain medium (working substance), and resonant cavity. The role of the pump source is to excite the laser working substance and pump the activated particles from the ground state to a higher energy level; the gain medium refers to the substance system used to achieve the population inversion and generate the stimulated radiation amplification of light. The resonant cavity is usually composed of two plane or concave spherical mirrors perpendicular to the axis of the active medium. It is a cavity in which light waves are reflected back and forth to provide light energy feedback.

Take the fiber laser as an example. The gain fiber is fixed between two fiber gratings to form a resonant cavity. When the pump light generated by the pump source passes through the gain fiber, the rare earth ions in the gain fiber will absorb the pump light and its electrons are excited. To a higher excitation energy level, the inverted particles are transferred from the high energy level to the ground state by radiation to output laser light from the core.

(2) Fiber laser has the advantages of high energy density and wide processing range, and its market share continues to increase

There are many types of lasers. According to the different gain media, lasers can be divided into fiber lasers, solid-state lasers, gas lasers, semiconductor lasers and so on. Different types of lasers have different application markets due to their different output laser wavelength, beam quality, output power and other parameters. The main performance parameter comparison of industrial lasers on the market is shown in the following table:

Carbon dioxide, solid-state, and semiconductor lasers have different performances, each with its own advantages and disadvantages. Because of its high power, high energy conversion efficiency, good output beam optical quality, good coherence, and stable work, carbon dioxide lasers are widely used in fields such as processing, communications, and scientific research. However, there are disadvantages such as large volume, complex structure, and difficult maintenance. Metal can not absorb 10.6μm laser light well, and cannot use optical fiber to transmit laser light. The solid-state laser has the advantages of large output energy, high peak power, simple and durable structure, and reasonable price. It has a wide range of uses in laser cutting, directional weapons, etc., but the thermal effect is very obvious, and the output efficiency is low. Semiconductor lasers are small in size, light in weight, reliable in operation, low in power consumption, and high in efficiency. They are widely used in optical fiber communications, photoelectric measurement, and military fields, but they are poor in directivity, monochromaticity and coherence.

In contrast, fiber lasers have more comprehensive advantages and are known as the "third-generation lasers." Compared with the above table, it can be seen that compared to solid, gas, and semiconductor lasers, fiber lasers have many advantages such as good output laser beam quality, high energy density, high electro-optical efficiency, convenient use, wide range of processable materials, and low overall operating costs. . Therefore, it is widely used in engraving, marking, cutting, drilling, cladding, welding, surface treatment, rapid prototyping and other material processing fields, and is known as the "third-generation laser." In the past ten years, the market share of fiber lasers has continued to grow. Its proportion in all industrial lasers has increased from 13.7% in 2009 to 51.5% in 2018, which is a clear leader compared to other lasers.

3. High-power laser processing will drive the industrial laser market to continue to grow

The global laser market is large in scale and is showing a steady upward trend. According to data released by Strategies Unlimited, the global laser market reached approximately US$13.75 billion in 2018, a year-on-year increase of 5.8%, and a compound growth rate of 11.1% in the past ten years. With the transformation of the aircraft and automobile industries to composite materials and the continuous increase in the penetration rate of high-power lasers, we expect the global laser market sales to continue to grow at a rate of 6.2% in 2019, and the market size will reach $14.6 billion.

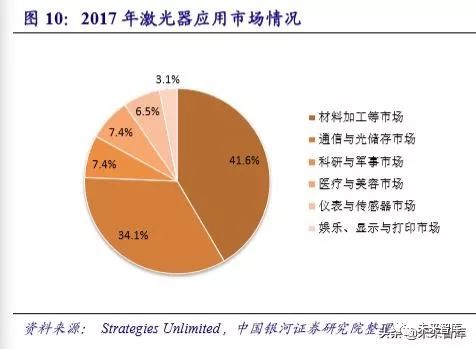

From the perspective of laser sales, material processing occupies a major position in the laser application market. According to data from Laser Focus World, in 2018, material processing and other segments continued to maintain the largest share of the global laser application market revenue, with a revenue scale of US$6.16 billion, accounting for 44.5%, an increase of 3.2% over the same period in 2017. Communication and optical storage are the second largest market, with a scale of 3.82 billion US dollars, accounting for 27.8%; scientific research and military, medical and beauty, instrumentation and sensors, entertainment and printing market share are 9.3%, 7.5%, and 7.4% respectively And 3.2%.

Specifically, high-power laser processing (cutting, welding) is currently the main application scenario. From a subdivision point of view, the applications of material processing include cutting, metal welding, marking, semiconductors, metal finishing and other fields. In 2017, cutting and welding applications accounted for 35% and 15% of global industrial laser material processing applications, respectively. They are currently the main application scenarios. Marking applications accounted for 15%, semiconductors accounted for 14%, and metal finishing applications accounted for 8%.

High-power laser processing drives the material processing market to grow steadily. According to Optech Consulting's consulting data, the global laser material processing market revenue in 2018 was $14.5 billion, and the compound growth rate from 2012 to 2018 reached 6%. As the penetration rate of high-power laser material processing continues to increase, we expect that the global laser material processing market will continue to grow in 2019, with revenue expected to reach US$15.6 billion.

The lasers used in material processing are mainly industrial lasers, which may continue to benefit. In 2018, the global industrial laser sales revenue was US$5.06 billion, a year-on-year increase of 4.2%, and the compound growth rate in the past ten years reached 17%, which was faster than the overall laser average. In the context of the continued growth of the downstream laser material processing market, we expect that industrial lasers will continue to maintain a relatively rapid growth rate.

4. China's laser industry maintains rapid growth and is optimistic about leaders with core technologies

(1) Revenue of domestic laser equipment market maintains high growth rate

Revenue from the domestic laser equipment market maintained a rapid growth rate. In 2018, the total revenue of laser equipment in industry, information, medicine, scientific research and other fields in the country reached 60.5 billion yuan, a year-on-year increase of 22%; in 2019, we expect the growth rate to remain between 16%-25%, and the market size is expected to exceed 75 billion Yuan. As a latecomer, the overall growth rate of China's laser industry is higher than the global average. In the long run, with the upgrading and transformation of China's economic structure to advanced manufacturing, we believe that the demand for industrial high-power laser equipment will maintain a high level of prosperity for a long time.

The domestic industrial structure is distributed in a pyramid. From the perspective of industrial distribution, domestic laser companies are mainly concentrated in downstream applications, and the overall structure is relatively scattered.

Downstream applications, except for the two industry leaders of Han's Laser (44.160, 0.20, 0.45%) and Huagong Technology (26.800, -0.20, -0.74%) (revenues exceeding RMB 10 and RMB 5 billion respectively), each sub-sector There are more participants. However, due to the relatively small overall market size of the sub-sectors, most of the laser companies are listed on the Science and Technology Innovation Board and the New Third Board.

In the midstream laser segment, domestic manufacturers are mainly Raycus Laser (64.010, 0.06, 0.09%), Chuangxin Laser and JPT (57.660, -1.20, -2.04%); in the operation control system, Baichu Electronics and Weihong Shares (66.620, 1.99, 3.08%) and Osendike occupy 90% of the low- and medium-power laser cutting control systems. International manufacturers in the high-power laser control system market still have an absolute advantage. In the upstream component link, some optical fibers have basically reached the level of international manufacturers, and core components such as pumps and chips are still dominated by imported components.

(2) The localization of low- and medium-power lasers has basically been completed, and the competition for high-power lasers has intensified

In the midstream segment, foreign fiber laser manufacturers still account for most of the market, but domestic substitution is the general trend. In 2018, the total sales of the national pipeline laser market exceeded 8.2 billion yuan, of which the IPG photonic market accounted for 50.3%. Ruike Laser and Chuangxin Laser, as the domestic leaders, still have a large gap compared with IPG.

However, in terms of trends, IPG China achieved revenues of US$629 million (approximately RMB 4.16 billion) in 2018, an increase of only 1.6% year-on-year; while Raycus Laser and Chuangxin Laser achieved revenues of 1.39 billion yuan and 6.6 billion yuan in mainland China during the same period. 100 million yuan, with a growth rate of 55.8% and 20.4%. In the context of the rapid growth of the domestic market, Raycus Laser and Chuangxin Laser's domestic market share reached 17.8% and 12.3% respectively in 2018, a significant increase from 2017.

The market for medium and low-power lasers is booming, and domestic substitution is basically completed. According to the power of fiber lasers, it can be divided into low power (<100W), medium power (≤1.5kW) and high power (>1.5kW) lasers. In recent years, the shipment of low-power fiber lasers has maintained rapid growth, from 13,000 units in 2013 to 110,000 units in 2018, with a domestic share of over 98%. It is expected that domestic brand shipments in 2019 are expected to exceed 125,000 units. Continue to take the lead. In terms of mid-power lasers, domestic shipments are expected to reach more than 15,500 units in 2019, and the growth rate will remain at 25%, which will continue to squeeze the share of imported manufacturers.

The difference lies mainly in high-power lasers, and market competition may intensify. Domestic brands of high-power (>1.5kW) lasers achieved market breakthroughs in 2018, with shipments reaching 2,000 units, accounting for nearly 40%, of which more than 300 6kW fiber lasers were put on the market. Against the background that domestic manufacturers have achieved technological breakthroughs, we expect that the market space will be further opened in 2019, and the localization rate is expected to exceed 50%.

The increase in localization rate will be accompanied by the downward movement of laser prices, and manufacturers' profits will be under pressure in the short term. Take the imported IPG fiber laser as an example. In 2016, the domestic price of its fiber laser was significantly lower than the price in 2012. Taking an imported 20W pulsed laser as an example, the price per unit in 2012 was about 9~ The 120,000 yuan fell to around 30,000 yuan, a drop of more than 50%. On the other hand, at that time, the domestic high-power laser technology had not yet broken through, and the import price was relatively strong, with a decline of only about 15%-20%.

With the breakthroughs of domestic manufacturers in the field of high-power lasers, the price competition in the industry in 2019 has become fierce. Taking Raycus Laser as an example, it adopts a passive follow-up strategy in terms of product prices and maintains a pricing gap with overseas manufacturers. Therefore, the gross profit margin has declined to a certain extent in the fierce competition.

(2) Laser components are still mainly imported, and localization is on the way

Optical devices such as chips, fibers, high-power fiber gratings, and heat sinks in the upstream link are important raw materials for the production of laser products. Related domestic industries started late, the technology is not mature enough, and the quality and stability are difficult to meet the market demand. At present, they are still mainly imported products (including purchasing from domestic agents). According to our analysis, the suppliers of the three major domestic laser manufacturers, except for a few domestic companies such as Keplin and Changguang Huaxin, are basically overseas companies or their agents.

Domestic leaders strengthened the proportion of domestic procurement. However, from the perspective of the amount of imported raw materials, from 2017 to the first half of 2019, Chuangxin Laser’s import procurement proportion dropped from 41.6% to 23.7%, and Jept’s imported raw material proportion dropped from 48.2% to 29.3%, reflecting the domestic leader Manufacturers are strengthening the proportion of domestic purchases.

Domestic optical fiber manufacturers have reached the technical level of foreign manufacturers, and optical fibers are gradually realizing import substitution. In the first half of 2019, the localization rate of passive optical fiber of Chuangxin laser pulse and continuous laser was 89.91% and 52.54% respectively, and the localization rate of passive optical fiber of JPT also reached 90%. As a gain medium, active fiber is more difficult and effective than passive fiber, and the localization rate is also increasing year-on-year. In terms of chips (pump source), domestic chips have reached a level that can be used normally, but they still have a certain gap with imported chips in technology. At present, leading domestic laser manufacturers mainly purchase Lumentum and Erlu laser chips and components. The link still needs to be broken. On the whole, China's laser equipment market has huge potential, and domestic substitution will continue to deepen. We are optimistic about industry leaders with core technologies. In the context of the “Made in China 2025” strategy, my country’s traditional industrial manufacturing industry is facing a deep transformation. The domestic laser equipment market will maintain a relatively rapid growth rate, with huge market potential. The rapid development of domestic manufacturers and the continued pace of domestic substitution in the laser industry chain have squeezed the market share of foreign companies. The downstream application link has formed a market pattern headed by the two leading companies in the Han's Laser and Huagong technology industries; the three domestic manufacturers of midstream lasers Ruix Laser, Chuangxin Laser, and JPT have already possessed core competitiveness, and domestic substitution is accelerating. The market share continues to increase. In the upstream component link, breakthrough development has been achieved in some links. In the future, it is necessary to continue to pay attention to the realization of independent controllability on the chip side. In summary, we are optimistic that leading downstream equipment companies will benefit from the market boom and the performance growth of domestic laser manufacturers with core technologies under the trend of domestic substitution.